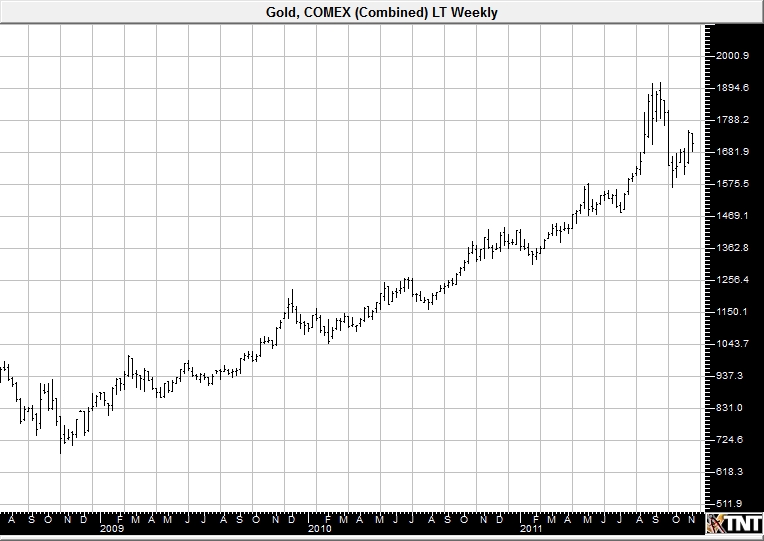

Currencies are coming into focus again this week. Japanese officials have made another move to devalue the yen to keep their exports humming. Like other commodities, precious metals are affected by currency changes. Whether it is shifts in monetary policy or developments in the European Economic Community (EEC), when currency relationships change look for gold and silver prices to be impacted. Let's take a look at the relationship between gold prices and global currencies in the chart below.

Gold prices have been traditionally used as a store of value and considered by many as the ultimate currency. Investors have developed a trust in gold when they become fearful towards other investment vehicles like stocks and bonds. Gold prices are typically valued in US dollars so as a result there tends to be an inverse relationship between the two. In other words, buyers and sellers of gold are influenced by changes in the exchange rate for US dollars. As the value of the dollar rises, then the purchase price of gold is often lower because you can now use those same stronger dollars to buy the same gold. Conversely, when the value of the US dollar declines, gold prices often rise.

Last week traders saw the US dollar trade substantially lower when heightened concerns over a Greek default were apparently averted. When the European Union announced an agreement was reached in principle to restructure Greek debt, traders holding short positions in the Euro scrambled to cover. That action forced the US dollar lower as the announcement strengthened the Euro in relation to the dollar while causing the price of gold and silver - along with other commodities denominated in US dollars - to move higher.

It is worth noting that the impact of that move was likely enhanced as fund managers moved out of shorts in the Euro and into long positions. Fund managers have had a rough year and since the end of the month was swiftly approaching their desire to have long positions on the books - or at the very least not be caught holding shorts - was obvious. Were those moves based upon sound fundamental reasons, or were they simply an over reaction?

From this week's perspective it appears as though that move was an over reaction since the news out of Europe has been negative regarding the deal. This has generated renewed fears among investors and as a result markets see investors now shifting back to the long side of the dollar. With the dollar gaining strength commodity prices have been under pressure - including the prices of gold and silver. Stock markets too have been experiencing the impact as have the value of US bonds, which have increased.

Economic events like these (and more importantly investor perceptions), fuel the ever-shifting relationship between currencies. In the current environment there is a noticeable increase in the frequency of knee-jerk reactions to whatever is the focus du jour in the 24 hour news cycle. The impact of the increased rate of the dissemination of information is obvious. Talking heads tend to value "breaking news" announcements, but in reality they have served to generate a tendency for swifter shifting between investment vehicles. This can decrease stability and invites increases in volatility and result in more stress on prices and investors. The game seems to have grown to be more a function of a race to positions, rather than a serious long term investment.

While this shifting back and forth is taking its toll, it only seems a matter of time before nervous investors seek alternative stores of value. Commodity prices, particularly among precious metals, have experienced investor demand. While silver has traditionally held an additional industrial use, much of the demand seen today is driven solely by investors. In other words, it is not a matter of industrial demand but rather demand driven by investors.

Jeffrey Currie of Goldman Sachs has said, "Gold is ultimately dependent upon real rates, which are a function of both inflation expectations and monetary policy. A top in gold prices will only become apparent when the risks of sovereign default are behind us with a clear and successful exit of the stimulus we've seen over the last few years."

The world is undergoing massive changes and numerous economic challenges. Sovereign debt is growing and seldom has the global economy seen such swift changes in the currency exchange rates. Driven by the whims and actions of nations and their leaders the outcome seems potentially disastrous. Central banks have been actively flooding the world with cheap money in an effort to cope with pending problems in their national economies. These banks printed money to escape liquidity problems and that by any definition is inflationary. The value of any currency is determined by changes in monetary policy. Inflation and deflation are phenomenons of central bank policy - and right now monetary policy is printing money.

As a result, more and more participants see cash moving into precious metals as gold and silver are chosen to fill their historic role: first as an inflation hedge, and more significantly as an alternate currency in a world where currency stability has become increasingly troublesome.

Summary

With few exceptions investors continue to believe that metals are not anywhere close to being finished moving higher in value. Yes, corrections must occur and most are healthy, but consensus has not yet suggested a top in precious metals. Maybe that is because gold cannot be created by central banking fiat. It remains scarce, difficult, and expensive to find and to mine. By many historic levels, gold and silver are still looking undervalued. Discounting for inflation, gold will have to exceed $2,000 per ounce to equal its previous peak value reached in 1980 - and that's without taking today's uncertain currency environment into account.

Disclaimer: The prices of precious metals and physical commodities are unpredictable and volatile. There is a substantial degree of a risk of loss in all trading. Past performance is not indicative of future results.