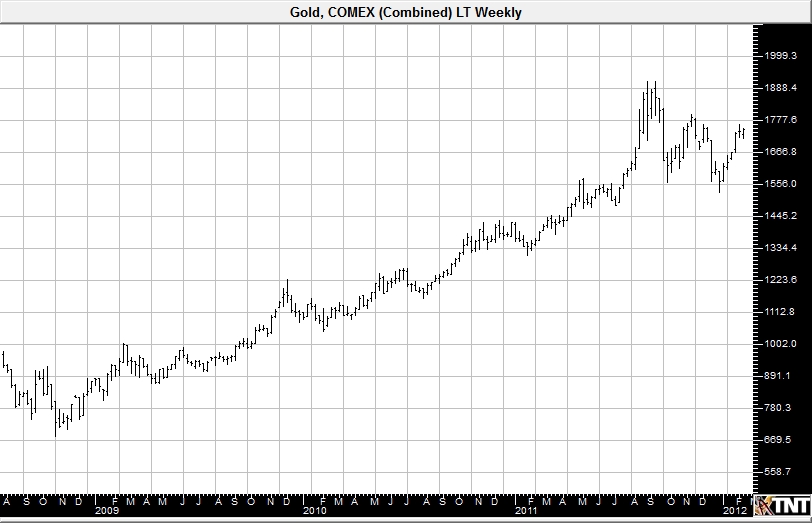

Precious metals have had an active and positive start in 2012. Gold is trading at some of the best levels since November, and the precious metals sector as a whole has performed well since the New Year began. Now that January has ended, what can we expect for these markets as 2012 moves forward? Better yet, what adjustments might make sense for some investors’ portfolios moving forward?

The age-old discussion of structuring an investment portfolio begins with evaluating and calculating an optimum investment selection mix, based on individual trading goals and risk tolerance levels. That frequently extends to precious metals in some form. The reason: precious metals tend to act as hedge, as a store of value, during times when other investments perform depressingly. Lately it seems that the bulk of investments are rising on a fresh wave of enthusiasm. There is every possibility that this is the result of forceful and repeated government stimulus. How long can that last? One bet is it will not last; not forever and likely not through 2012.

After the crash in 2008, first came the Obama/Bush stimulus spending package, succeeded by Quantitative Easing (QE) 1, QE2, and Operation Twist. Following the most recent Federal Reserve Open Market meeting, Bernanke declared that interest rates would be kept low through 2014. So what came from all this? Slower growth, minor job creation, higher energy and commodity costs, (are commodities signaling inflation?), continued housing devaluation, and virtually no new business start-up entrepreneurship. What is left; more of the same?

Both the U.S. and European governments have been extraordinarily aggressive at employing tactics to combat the economic slowdown, but could be running out of ammo. The accelerated monetary policy wielded to prevent a brutal recession has sapped the strength of the Fed. Consumers remain cautious, some even deeply frightened. Businesses have retrenched. The collection of creative recovery tools via fiscal and monetary that have been applied have proved relatively ineffective under the circumstances. It seems highly suspect for the pace of the monetary easing required to continue without an offsetting escalation in inflationary forces. Central banks may possess the ability to print money, but it is doubtful that they possess the resources and economic credibility to play as vigorously as they have been doing. The weaknesses may eventually be repaired, but their ammo is running out as quickly as investor confidence.

This has changed the traditional conception of the American, and now global, marketplace. The global financial system has grown even more inter-related and lacks a smooth clean regulatory framework. Searching for stability, the U.S. and some European governments have made a dramatic shift towards nationalizing their financial sectors to such a degree that they are almost unrecognizable. The resulting sovereign debt has become the daily big issue. The role of government in the economy is larger than it has been in the average investor's lifetime, while the role of the private sector is far smaller.

So what happens with such a tough road ahead for global economies? With such strong headwinds for stocks it may be that the average portfolio could look at reweighting itself toward more precious metals. Equities have been surprisingly resilient, but the framework still does not suggest the prospect for sustained growth in the immediate future. Certainly U.S. unemployment numbers, GNP, and other leading indicators have been better than expected and contributed to stock market gains, but markets do not just go straight up. Healthy markets tend to adjust and correct.

Being an election year in the U.S., it is not altogether unusual for indicators to be received in positive fashion. Historically, with few exceptions, the modern economy has performed well during election years. Yet what steers the boat has less to do with the performance during election years than it does with common sense. The fiscal policies have been repetitive and aimed at sparking the engine, yet it must eventually run on its own accord. Market and fiscal trends are apt to change, sometimes violently.

All of the newly-printed fiat money has provided much-needed relief. Though a short-term improvement, such behavior can only serve to depreciate currencies and inflate commodity prices, especially in metals. As currencies float, it is not as easy to see the subtle moves made by inflation. Fiat currencies makes hard asset commodities, such as oil, gasoline, and food cost more as a result. On the other hand, metals benefit as they are held as a store of value. As other investments get punished, consumers become fearful, and the prospect of business growth slows, metals are likely to take center stage.

Summary

Equities are likely running out of steam - volume has been lagging and bull markets need fresh investors to fuel rallies. Investors would not be wrong in considering the moment ripe to restructure and reevaluate their portfolios. If inflation continues to accelerate, metals could step in and fill the stocks’ void. Precious metals could also offer long-term liquid hedges against the loss of purchasing power in other currencies, and they look set to remain the ultimate currency, especially in the current economic climate.

Disclaimer: The prices of precious metals and physical commodities are unpredictable and volatile. There is a substantial degree of a risk of loss in all trading. Past performance is not indicative of future results.